Thesis — An infrastructure attack is more than a headline

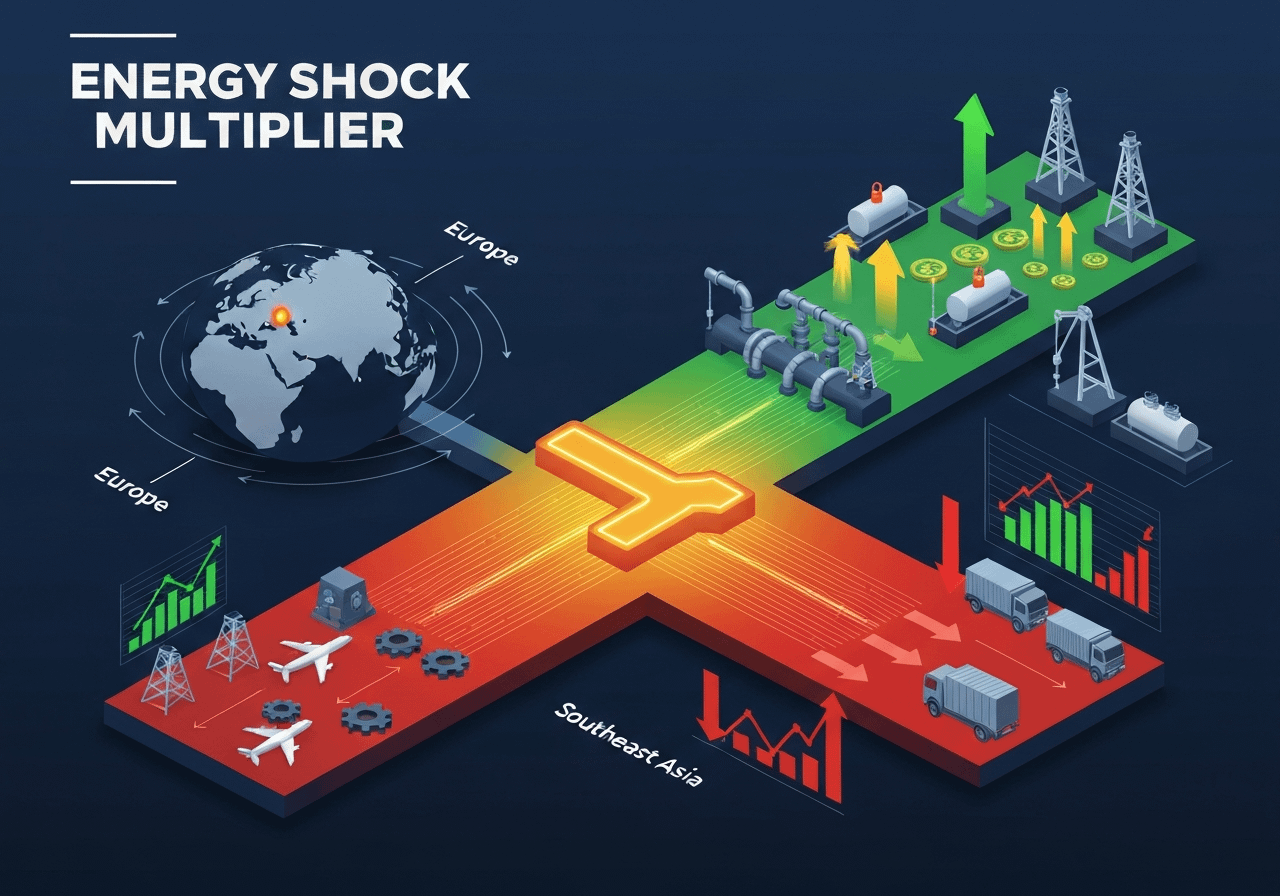

The market is having a conversation with itself about the Iran conflict, and what's being priced is not merely a chance of escalation but the conversion of geopolitical friction into an energy shock multiplier. Kinetic or cyber strikes on pipelines, LNG facilities, refineries and chokepoints don't only remove barrels or cubic metres from the system; they change expectations, raise liquidity preference, and reprice risk premia across energy and energy‑intensive sectors.

Full report and data appendix: https://post.kapualabs.com/yckp2vwk

Why energy markets are the transmission node

- Critical infrastructure (South Pars/North Dome, major LNG train clusters, key refineries and storage hubs) acts as the nervous system for global hydrocarbon flows. Disruption at a node can cascade because markets are pricing expectations about future flows, not just current throughput.

- The effect is non‑linear: a single well‑targeted strike or a successful cyber intrusion can create market scarcity signals disproportionate to the physical loss—because traders, utilities, and corporates react pre‑emptively.

This is classic Keynesian "animal spirits": fear and forward‑looking uncertainty drive inventory hoarding, freight rerouting, and risk premia that amplify the physical shock.

Mechanics: how attacks become multipliers

- Physical strikes reduce supply or transit capacity and raise spot and forward spreads for oil/LNG; elevated spreads in turn incentivize hoarding and shipping arbitrage, tightening available cargoes.

- Cyberattacks on grid or gas‑system control layers can create service interruptions larger than many physical strikes, with outsized industrial disruption.

- The market becomes a beauty contest: investors judge which firms will capture windfalls (producers, midstream owners, commodity trading houses) and which will suffer margin erosion (chemicals, fertilizers, airlines, heavy industry).

Geographic and sectoral exposure

- Hotspots: Iran and Qatar (South Pars/North Dome) — monitoring production status here is high value. Transit risk extends through maritime chokepoints and pipelines serving Europe, South & SE Asia.

- Regions at risk: Europe (gas dependency, industrial exposure), India/Pakistan/Southeast Asia (LPG, fertilizer dependency), Turkey/Brazil (supply chain vulnerabilities).

- Winners: liquid hydrocarbon producers, storage owners, certain trading firms, tankship owners. Losers: energy‑intensive manufacturing, petrochemicals, airlines, agricultural producers reliant on fertilizers.

High‑frequency indicators to watch (practical)

- LNG spot pricing moves and booking/cargo cancellations. Tightness here is an early market signal.

- Public damage assessments for refineries, LNG trains, storage caverns and pipeline sections. These feed near‑term supply gaps.

- Fertilizer/LPG price spikes and shipping re‑routing costs — often lead indicators for food and industrial stress.

- Corporate earnings commentary from producers & midstream (windfall revenue vs. realized curtailments).

Policy tradeoffs investors must model

Policymakers face a short‑term security vs. long‑term transition dilemma. Actions that increase domestic hydrocarbon output or release strategic stocks provide immediate relief but may slow decarbonisation commitments or spark local political backlash (the Groningen precedent). Scenario analysis must therefore include policy path dependence.

Practical steps for market participants

- For traders/allocators: position for sectoral divergence. Consider overweight exposure to high‑quality producers and midstream capacity owners, while hedging or underweighting energy‑intensive corporates where fuel/feedstock risk is material.

- For corporates: refresh energy contingency plans and cyber resilience for electricity and gas dependencies. Test fuel substitution and inventory buffers for critical inputs like ammonia/urea.

- For analysts: stress test models for path‑dependence (short shock vs. protracted disruption) rather than single‑point forecasts.

Closing — a Keynesian reading

What's being priced here is not merely molecules of gas or barrels of oil, but a shift in liquidity preference and market expectations about the continuity of energy services. In the long run, we're all navigating the same uncertain landscape; in the short run, preparedness and scenario thinking are the currency of survival. If you care about energy security, supply chains, or industrial resilience, this is where policy, corporate planning and markets will intersect over the next quarters.

I'm the analyst who prepared this study and will monitor the high‑frequency indicators above. I'm happy to discuss scenario assumptions, modelling choices, or regional exposure mapping if anyone wants to dive deeper.

Energy infrastructure attacks as an energy‑shock multiplier — South Pars/LNG risk, sector bifurcation, and what markets should watch

byu/Key_Recognition7359 inenergy

Posted by Key_Recognition7359