– Core customer makes <$35k/yr. Gas at $4.50+/gal eats their savings before they even walk in the door

– Stores are rural. High gas = fewer trips. The discount doesn't matter if the drive costs more than you save

– Management guided $7.10-7.35 EPS two days ago. That guidance assumes oil isn't at $90+. It is. Guidance is already dead

– Every $10/bbl oil sustained for a quarter shaves ~$0.15-0.20 off EPS. Do the math on a $20+ spike

– DG runs 20,000 stores with a massive truck fleet. Diesel eats gross margin directly. They don't have Walmart's scale to negotiate it away

– Last time they missed on "consumer health" (2024), stock dropped 32% in a single day. Algos remember

– If Iran drags on 5 more weeks, mid-April negative pre-announcement is on the table. Algos will front-run it to ~$105

– 80%+ of sales are low-margin essentials now. More volume, worse margins

– Smart money already rotating out — Victory Capital cut 50%, Grantham Mayo cut 70%

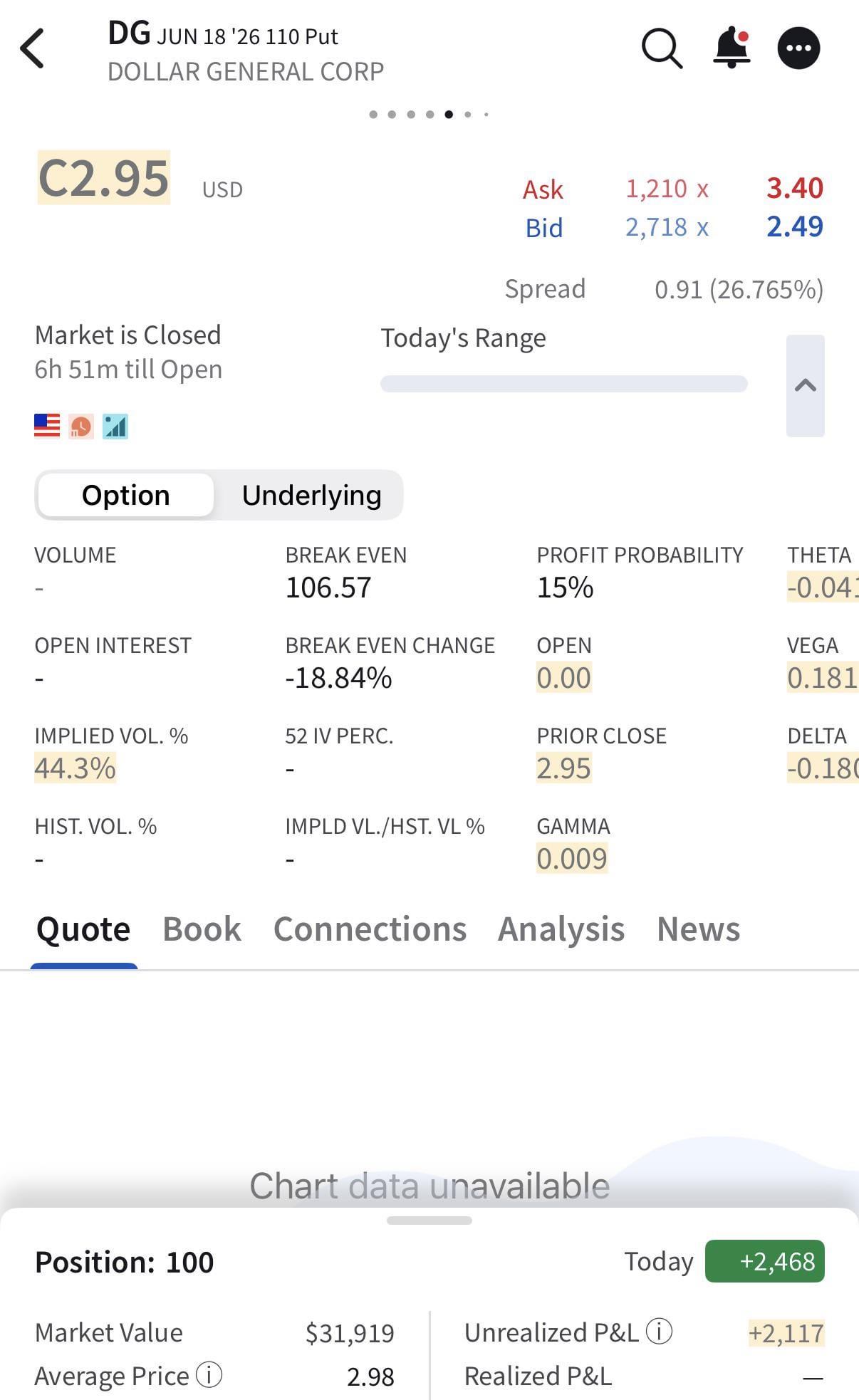

Position: long 100 x $110 June ‘26 put contracts

https://i.redd.it/00u9qyja2rpg1.jpeg

Posted by ApartmentVegetable77

6 Comments

[deleted]

https://preview.redd.it/66lxgzo54rpg1.jpeg?width=959&format=pjpg&auto=webp&s=3f8c2f52685b7f89a3f6826c9ce1d99af3770390

you did all this research just to get rugged anyway

War and inflation and you bought puts on the only place that we’ll all be able to afford to shop at soon?

Witness him

Cool. Implied Vol is very very high though. I think puts on india might actually be priced cheaper despite being the much simpler thesis (puts on a country with poor consumer purchasing power and high oil dependence).