THE TLDR FOR THE SMOOTH-BRAINED:

Planet Labs takes pictures of Earth from space every single day. Governments, militaries, hedge funds, and farmers pay them a lot of money for those pictures. Yesterday, they reported their first full year of profitability. The backlog just hit $900 million. The stock ripped 31% today, and I think this is the beginning, not the end.

Let me explain.

WHAT DOES PLANET ACTUALLY DO

Imagine Google Maps, but it updates every 24 hours instead of every few years, and the CIA uses it. That’s basically Planet. They operate the largest constellation of Earth observation satellites on the planet (pun intended), imaging virtually the entire surface of Earth daily. Governments use it to track troop movements. Hedge funds use it to count cars in Walmart parking lots. Farmers use it to monitor crop health. The use cases are genuinely limitless and they expand every year with AI.

They’re not trying to be SpaceX. They’re not trying to colonize Mars. They’re the picks-and-shovels play for everyone who needs to see what’s happening on Earth in near real-time. Boring? Maybe. Investable? Let’s talk.

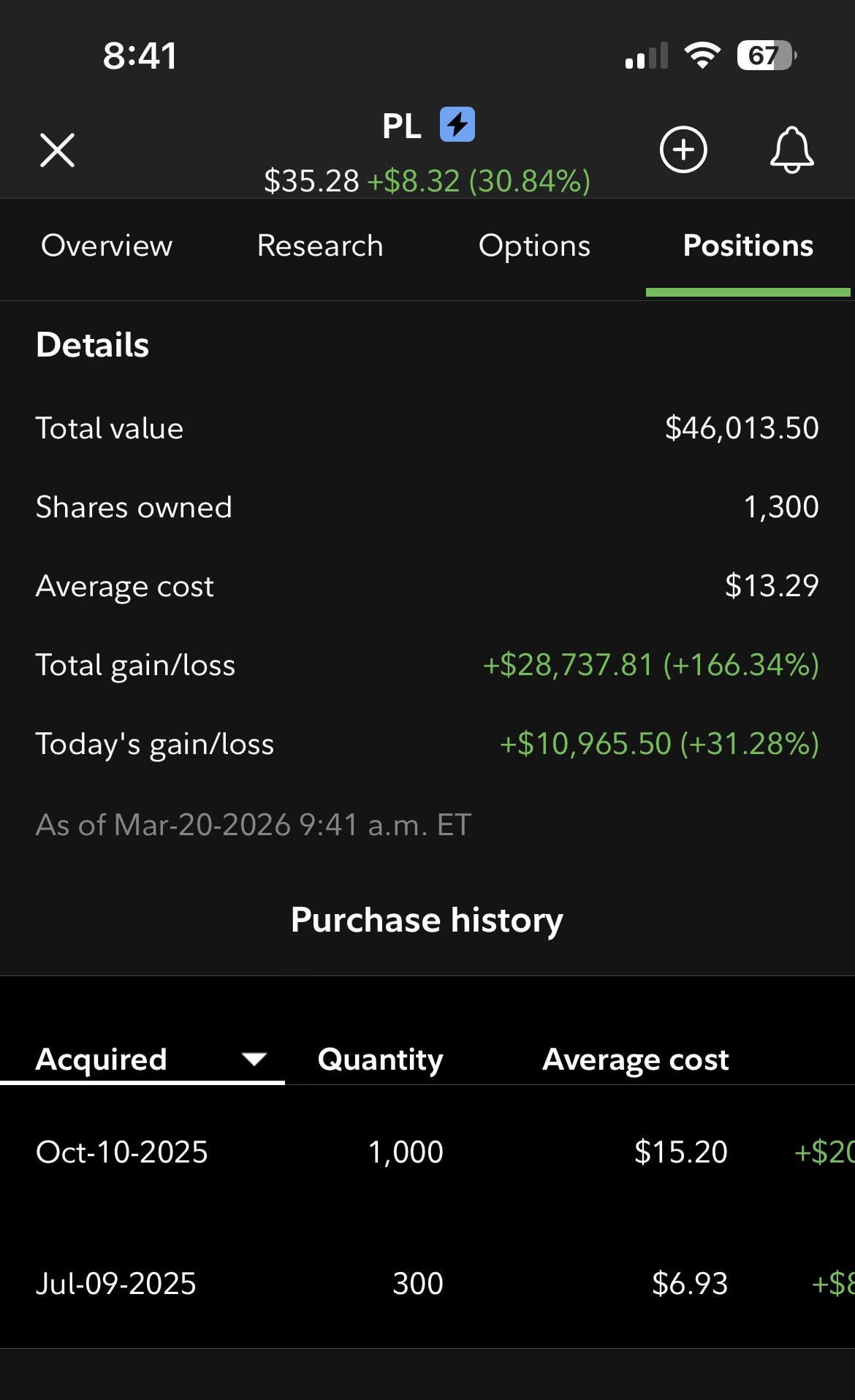

THE NUMBERS (Fresh from YESTERDAY’S earnings call)

Full year revenue came in at a record $308 million, representing approximately 26% year-over-year growth. Q4 alone grew 41% year-over-year.

For context, this company was growing at \~11% YoY a year ago. The acceleration is real and it’s not slowing down.

End-of-period Remaining Performance Obligations (RPOs) hit $852 million, up \~106% year-over-year. About 34% of that converts to revenue in the next 12 months, and 65% within 24 months.

Translation for the non-finance crowd: RPO is essentially money they are contractually owed. It’s not a pipeline or a wish. It’s signed contracts waiting to be recognized as revenue. At $852M in RPOs vs. $308M in annual revenue, they have nearly 3 years of revenue already locked in and growing.

Total backlog hit $900 million, up 79% year-over-year.

This was also their first full fiscal year of non-GAAP profitability and positive free cash flow.  This is the inflection point. The “are they going to survive?” question is off the table. Now it’s “how big can they get?”

THE GUIDANCE (Why I’m Actually Excited)

For FY2027, management guided revenue of $415–$440 million. For Q1 alone, they’re guiding $87–$91 million.

That’s ~35–43% revenue growth projected for next year. On top of a year where they already grew 26%. If they hit the midpoint of guidance, this is a company nearly doubling revenue in two years while achieving profitability.

THE GOVERNMENT CONTRACT MOAT (The Part Most Retail Investors Sleep On)

This is where the story gets genuinely compelling. Planet isn’t just selling imagery subscriptions to random companies. They are becoming infrastructure for Western defense.

In the past year alone, they signed a €240 million multi-year deal with Germany, a nine-figure agreement with Sweden, and received awards from NATO and the U.S. Missile Defense Agency.

They were also selected as a prime contractor under the Missile Defense Agency’s SHIELD IDIQ contract vehicle, which carries a ceiling of $151 billion.

Read that number again. $151 billion ceiling. Planet is now a prime contractor on one of the largest defense contract vehicles in U.S. history. They won’t capture all of it, but being on the approved vendor list for a $151B program is not nothing.

The Defense & Intelligence segment specifically showed over 50% growth, leading all business segments. As geopolitical instability continues to be the theme of the decade, governments are spending more on situational awareness, not less.

THE GOOGLE/NVIDIA WILDCARD (Free Lottery Ticket)

Here’s the part that could make this a completely different company by 2028 if it works.

Planet has partnered with Google on Project Suncatcher, an R&D initiative exploring scaled AI computing in space. The goal: put Google’s Tensor Processing Units (TPUs) directly on satellites, powered by continuous solar energy, to run AI workloads in orbit.

They’ve also partnered with NVIDIA, claiming 100x speedup on certain data processing tasks.

To put this in plain English: right now, Planet takes photos in space and beams them down to Earth for processing. Project Suncatcher would mean the AI analysis happens in space before it even hits the ground. Faster, cheaper, more scalable. If this works, Planet doesn’t just sell imagery; rather, they become orbital AI infrastructure. That’s a completely different TAM.

This is not in the current price. It’s upside optionality, not a base case assumption.

THE BEAR CASE (Being Honest)

∙ GAAP net losses are still real. Q3 saw a net loss of -$59.2 million attributable to common shareholders.  They’re profitable on an adjusted EBITDA basis but GAAP profitability is still out.

∙ Management noted that roughly 85% of annual contract value is annual or multi-year contracts, down from prior periods, as more large, shorter-term government contracts have been signed recently.  More lumpy revenue is a risk.

∙ Competition exists: Maxar, Airbus, and increasingly, startups. The moat is real but not impenetrable.

∙ The stock is up significantly since last year. You’re not getting in at the bottom.

THE BULL THESIS IN ONE PARAGRAPH

Planet Labs is transitioning from a scrappy satellite startup into a mission-critical defense and intelligence infrastructure provider, with a $900M backlog growing at 79% YoY, FY2027 guidance of $415–$440M, partnerships with Google and NVIDIA on in-space AI computing, and today just achieved its first full year of profitability. The stock is still under $30. If they execute on guidance and even one of the moonshot partnerships bears fruit, this looks cheap in hindsight.

TLDR: Satellite company that images Earth every day just had a blowout quarter, has $900M in backlog, is now profitable, is under contract to support Western defense across Germany, Sweden, NATO, and the U.S. Missile Defense Agency, and is building orbital AI data centers with Google. Stock ripped 31% today. Still under $40. Not financial advice. 🛰️

Positions: Long $PL shares. Do your own research. I am not a financial advisor. I learned most of what I know from satellite imagery of Wendy’s parking lots.

https://i.redd.it/4igxs7chg7qg1.jpeg

Posted by redpillsbluepills

11 Comments

Nice 🖕🖕

Bro wrote a novel so I can lose money faster

Ah yes, another one of those posts written **after** the stock is up over 30% on the day. So useful.

I bought a ton of calls before their earnings super happy with the results. Been holding rocket lab for like 2 years now

This is WSB, there is no need for your stupid ass disclaimer about not being a financial advisor. That said, congrats and fk you

Hi I sold at $7

sold a crap ton of puts last night for an over night success. like stealing candy from a baby.

OP explain to me how they have a moat, but don’t have their own launch vehicle to put their satellites into space?

Owned them through 2024. Sold at 4$ 🙁

Same story with pltr

DD on a position you bought a year ago and you’re already up. This is super gay. Where was the DD post a year ago? God how do the mods allow this shit

https://preview.redd.it/g2irm25tp7qg1.jpeg?width=1206&format=pjpg&auto=webp&s=1a4fa236a2a299f29c8ce97cbaff5c150028c95c

BOUGHT THIS $19 CALL BACK IN AUGUST 2025.

DIDNT MOVE FOR 3 MONTHS.

DECIDED TO SELL IN NOVEMBER AND DEPLOY THE FUNDS INTO ANOTHER PLAY.

ANOTHER 3-4 MONTHS LATER AND IM SAD BOY.

OPTION CHAIN SAYS THIS IS WORTH ABOUT $1800.

WOULDVE BEEN A 18x