Hi everyone,

I've been working on a deterministic approach to quantify market fragility beyond simple price action or sentiment indices. My focus is on identifying Market Regimes (Normal, Stress, Critical) by analyzing the underlying 'structural plumbing' of the network.

The Methodology: Instead of using generative AI or black-box models, I rely on:

- Volatility Clustering: Measuring the persistence of abnormal variance within specific timeframes.

- Liquidity Resilience: How the order book depth reacts to systemic shocks.

- Carry Density & Kappa: (Ici, tu peux mentionner tes termes techniques de chercheur).

Observations: Through backtesting, it appears that structural stress often builds up in the liquidity layers days before it reflects in the spot price. I'm curious to hear from other researchers here:

- What are your thoughts on using deterministic regime-switching models vs. stochastic ones for risk monitoring?

- How do you factor in systemic correlation when the 'Critical' threshold is reached?

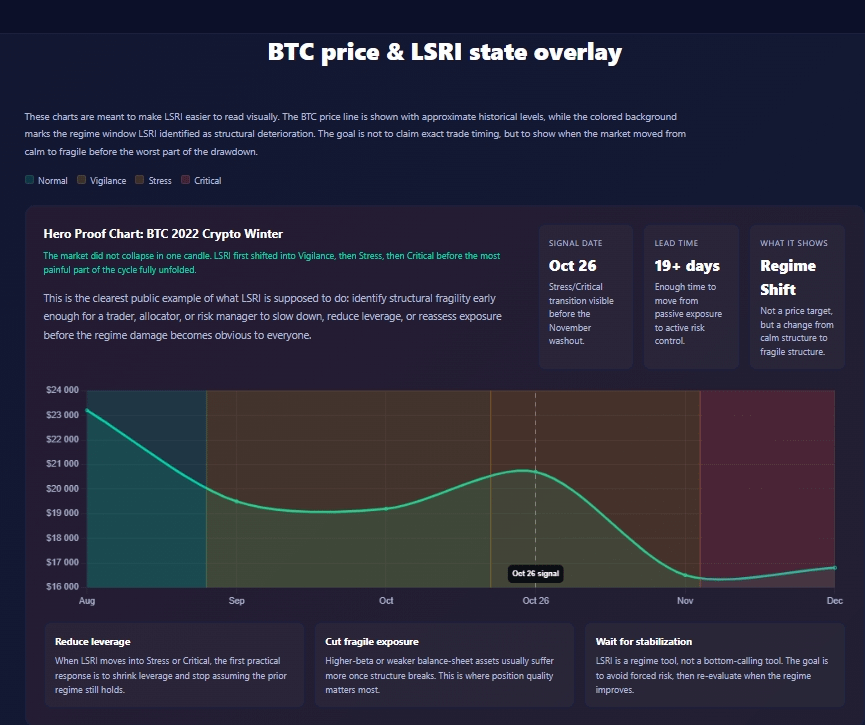

Data Visualization (Backtest): https://imgur.com/a/aJAisXY

I'm looking for a purely technical discussion on the logic of regime identification. Any feedback on the mathematical framework would be appreciated."

Detecting Market Regime Shifts through Volatility Clustering and Liquidity Stress Analysis.

byu/Steflavoie65 inCryptoTechnology

Posted by Steflavoie65