Intel stock is one of the highest in the latest decade and close to all time high.

Now I will point into the factors that make Intel overvalued even considering the US investment, Nvidia investment as well as an optimistic Google, Nvidia as well as other marketshare of fabbing chips.

1) Intel has slimmed down considerably in the last 5 years, it was forced to sell it's RAM, flash storage as well as many other businesses that had a good chunk of marketshare. Currently intel has basically 2 main businesses, the Cpu (consumer and datacenter) and the fab services.

2) Intel latest node, even if it's using latest ASML litography machines and is cutting edge, still lags behind last gen of TSMC that uses older litography tools.

The nm and node names or w/e are marketing tactics, if you check the actual density on wikipedia or semi wikis you can see that intel 18A on latest lito ttools is almost 20 % less dense than equivalent TSMC on last gen tools, so unless Intel sells at a very competitive price, there is no particular reason so choose intel over TSMC currently.

3) It is not easy to switch fabs Intel has been very vertically integrated over the years, and they were struggling to get Fab customers because of needing different tooling to model the CPUs and different waffer sizes, they had to do compatibility tools and whatnot, but TSMC moat is also in the software and processes not only in them having leading edge nodes. TSMC has the CUDA equivalent for Intel

EDIT 3.5. Intel is currently fabbing some tiles of their older CPU series as well as their ARC GPUs on TSMC as well.

If Intel 18A is so great, why don't they fab their own shit on it instead? don't tell me Intel will sell their capacity at higher prices than TSMC to justify paying TSMC to fab their shit.

Intel 18A is not production ready, these deals are farts, the same way OpenAI did the RAM waffers that can be canceled by either party at any time.

4) Intel not being a pure player in fabs makes companies reluctant to use them, the same thing happened to Samsung.

Intel is a competitor for many of the companies that want to fab on their machines, but furthermore companies are also afraid of IP theft. This happened with Samsung before after fabbing Apple stuff magically improving and "borrowing" stuff for their own Cpus.

5) Intel 18A has bad yield issues. The market reacted positively to Intel saying they will do budget cpus on 18A, but not only are these less profitable, but the reason they are doing this is to hide bad yields.

By intel own numbers last earnings, Intel 18A won't be production ready for fabs until next year at best

Now let's talk numbers, and synergy.

Intel advantage for many years until TSMC and ARM domination was vertical integration, they designed and fabbed their own shit, so they had insane cost effectiveness.

Now intel wants to become a Fab, and also continue to make chips (unless they split like AMD did)

This is problematic for various reasons, first of all Fab might not be as lucrative as selling CPUs, but also you are competing on capacity with your clients.

Also Intel main profit comes from selling CPUS, for consumers and datacenters.

For consumer it's been grim for a while as the PC market is shrinking as it's being slowly eaten by tablet/phone market.

Used to be you needed a PC to read your emails or watch youtube or check facebook or w/e your mom did in her 20s, now you can do these things on a phone/tablet.

Furthermore apple's macbooks are very competitive on price, and with them being very vertically integrated and having preferential prices with suppliers such as TSMC it's very hard to compete.

On the datacenter the AI demand gave Intel a lifeline, but it's still not looking good because unlike Nvidia there is no CPU moat.

It's even worse than this, most cloud providers are switching to ARM, and have custom ARM chips, that are more cost-effective than intel, the world is slowly switchin away from x86

Now back to earnings, I don't expect Intel to deliver, and furthermore their guidance for the year will be bad.

I expect a roughly 15% crash in the days following earnings.

Now people will claim what they want about AI and market irrational, but AI is economically on shaky ground now, especially with OpenAI IPO in peril as well as Oracle being in debt and their financial and profitability is questionable.

No sane fund will yolo on intel.

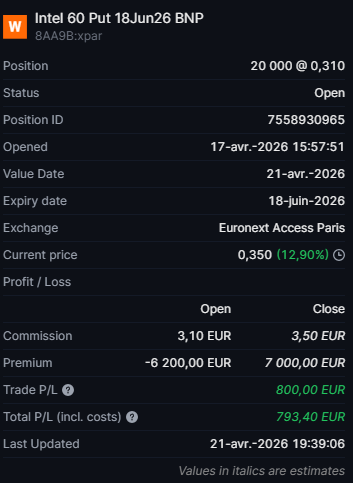

Position: 30k Intel 60 Put expiring 18 June : https://i.imgur.com/gPrfrn3.png

Intel DD : Earnings play, crash

byu/AppleTrees2 inwallstreetbets

Posted by AppleTrees2

29 Comments

Nana, please, forgive this poor soul. Not his port tho.

Bullshit. Calls. You’re betting against a 🥭 propped up company.

I’m not sure I would bet against a chip maker in an AI bubble right now. You’re correct about AI being on economically shaky ground at the moment, but the market doesn’t care either.

In before share buyback to keep the circle jerk going

People won’t get off this stock…

man you really went deep on this one lol. the fab competition stuff is real though, like trying to compete with tsmc when they already have all the relationships locked down seems brutal

been watching intel struggle with yields for ages now and that 18a situation doesn’t look great. also the whole thing about being competitor to your own fab customers is such a weird spot to be in

geometry dash taught me that precision matters and intel’s precision on these nodes just isn’t there compared to competition. when you’re missing the timing windows this bad it gets expensive fast

good luck with those puts, earnings season always gets spicy

You’re ignoring national security in the most important forward looking sector. Intel cannot and will not fail, we won’t let it. Also you’re just going to ignore spacex/tesla/intel gigachad partnership? This bitch can’t lose

i think puts are the move as well, its already gone up so much since the dip on 3/30, wouldn’t be surprised that it is priced to perfection and wallstreet is waiting to sell even on a beat

So many half-truths here and some outright incorrect statements.

Calls.

Yields rumored to be 75 for 18a, not sure about the other node variants. Probably trailing behind in the 50/60s which will be used for external production. Other companies like Google.

Any takes on the AI rush? It seems like they are all chasing the singularity but will run out of stream before acheieving anything.

Bro Intel is one of the top 3 semiconductor manufacturers in the USA. They employ tons of people, have manufacturing facilities that take years and billions to set up already up and running, experience, and backing of the US government. On top of all that, add huge demand for chips/servers due to data centers popping up like weeds throughout the world to support AI integration into modern society. I wouldn’t be betting against Intel.

I’m gunna sell 1/2 my shares on the earnings pop and rotate into MSTR. The party can’t stop.

Thank you for this post, inverse wsb might just work again 😅

No TL;DR? I’m assuming you said calls

If it’s such a bullshit company why is it up 75% ytd?

Is that 7 million Euro in puts!?

Edit: nm, this regard read it wrong

Best case you make a limited profit, worst case your ass gets blown out… nice play 😎

All the comments doubting this guy.

This gonna print

I think you’re right short term, but I think Intel is gonna moon long term.

You’re right that TSMC is ahead, but Intel closed the gap quite some compared to what it was. Before, it didn’t even make sense to get Intel chips as they were so behind it wasn’t cost efficient at all. My take is that there’s so much chip demand that both TSMC and Intel are gonna eat good.

Yea, but they’re about to announce nvda, amzn, Matt, goog, amd, TSLA etc as major foundry customers. Not to mention building terafab for our lord and savior, Elon.

I have two childhood friends (well, they’re cousins) one works for intel in Malaysia and the other one moved to South Korea to work for Samsung.

Both of them told me they’re buying Intel.

I’m gonna bet on inverse Nana here.

Calls it is. Every time a WSB user thinks they know their stuff, it always fails. THANK YOU FOR REAFFIRMING MY CALLS LOL.

Didnt read. Calls it is

https://preview.redd.it/o3iveapgalwg1.jpeg?width=1125&format=pjpg&auto=webp&s=39f4f8cb62cbe5879a1fa2fc4b62976e080b588a

Everything you said is true but people keep buying this shit up after the terrascam and Google partnership announcement

A 15% crash isn’t that bad.

OP is regarded

But boy do I love the sudden shift in sentiment on WSB from last years. Hindsight 20/20 mfs.

https://preview.redd.it/3bbffce4clwg1.png?width=1133&format=png&auto=webp&s=e983ffa86f44f23ea3e40f739198ff81a3d13d83

May the best man win (roughly same amount of cash – opposite direction)