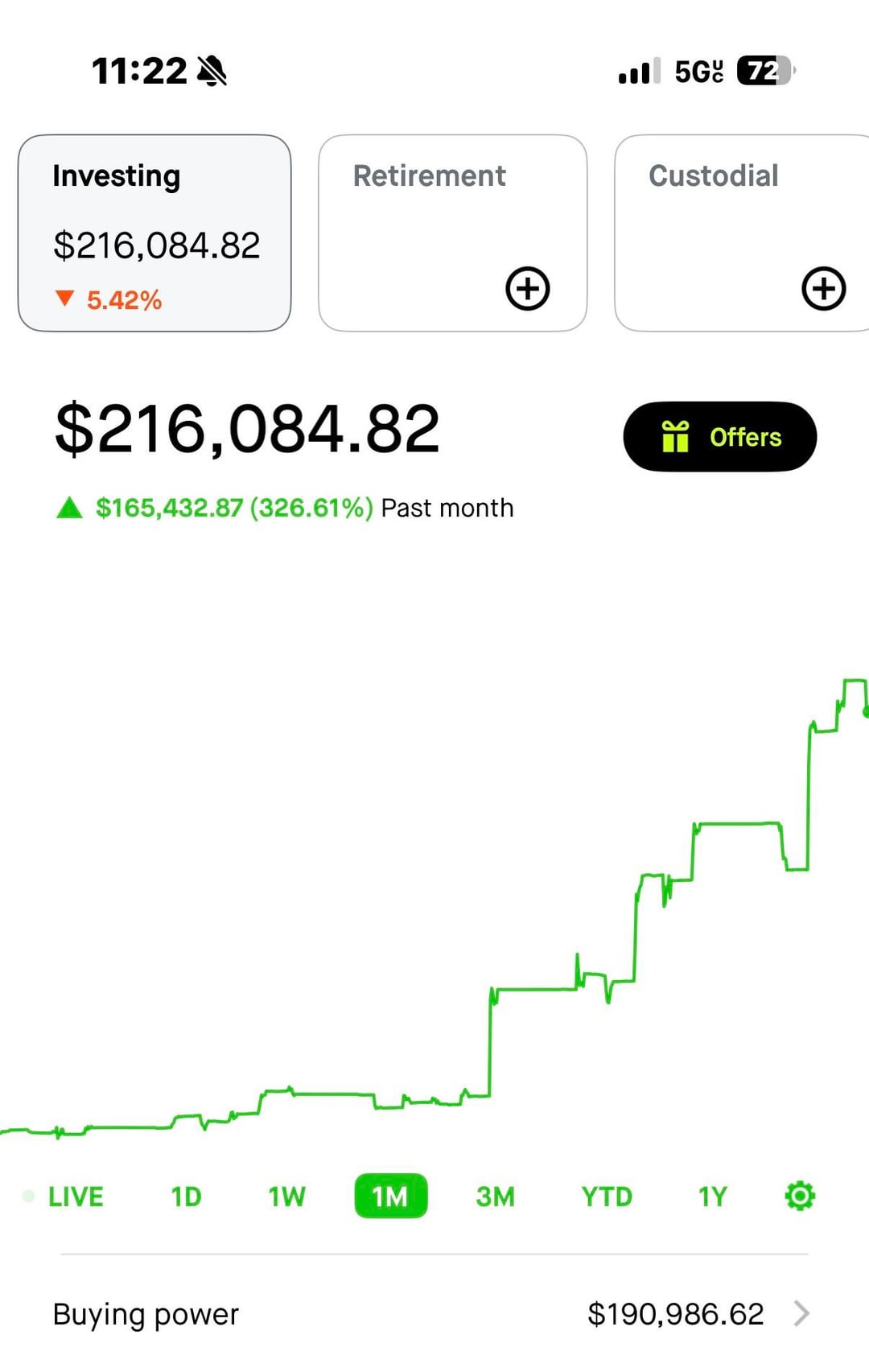

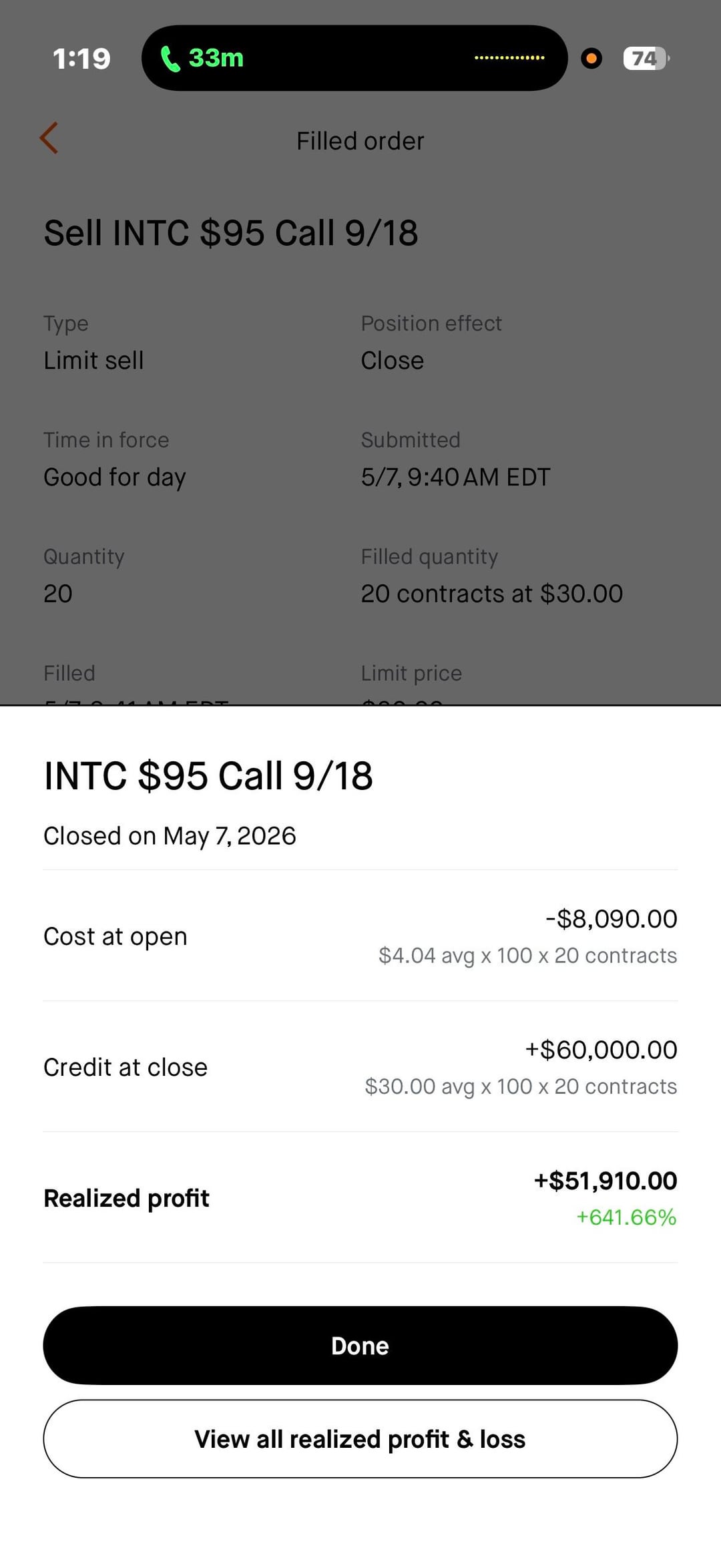

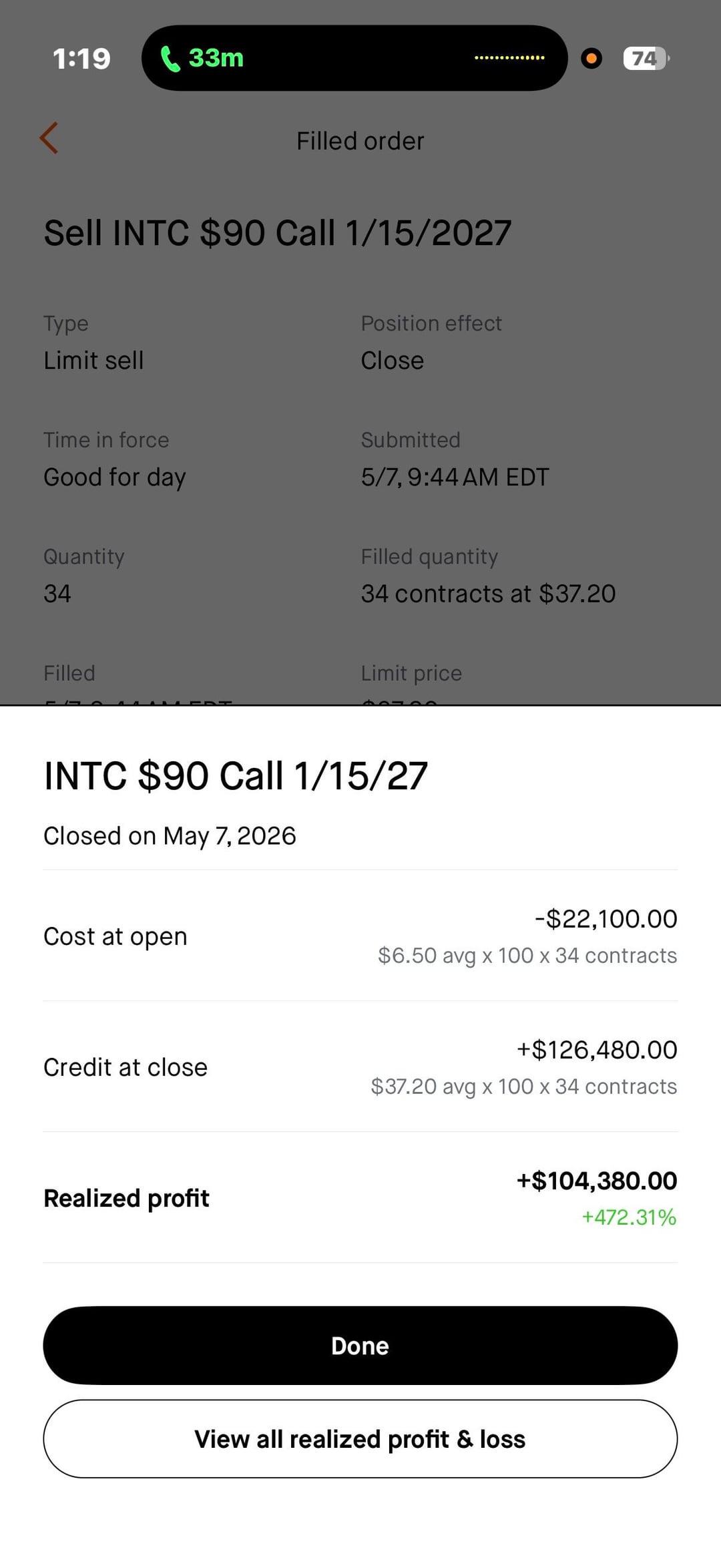

Opened the position last month when it was 62, I’m out at the moment, still bullish on INTC, will buy back if it pull back

https://www.reddit.com/gallery/1t6h848

Posted by zhumail134

Opened the position last month when it was 62, I’m out at the moment, still bullish on INTC, will buy back if it pull back

https://www.reddit.com/gallery/1t6h848

Posted by zhumail134

9 Comments

My cost basis is $29.84/share. I want out but tend to sell too soon and miss additional runups, so torn on this one.

Nana is that you?

bought in at 28, sold at 33, bought back at 30, now just staring at my screen like what did i do lmao

I’m trying to figure out whether AI infra is still one of the best long-term themes in 2026, or if the market is starting to price in slowing growth / margin compression.

Names like ARM, Fabrinet, and Teradyne all have real AI exposure:

ARM → AI CPUs / power-efficient compute

Fabrinet → optical networking / photonics

Teradyne → AI chip testing

But despite strong earnings and AI demand, these stocks have been selling off hard lately.

My current take:

AI demand itself still seems very real

Inference + agentic AI probably increases infrastructure demand long term

But the market may now care more about durable margins and bottlenecks instead of “anything AI”

It feels like we’re moving from:

“AI buildout euphoria”

to

“Which companies actually keep pricing power?”

I’m wondering:

Are these pullbacks opportunities?

Or are these names becoming cyclical semiconductor/hardware plays again?

Which AI infra layers do you think still have the best long-term economics?

Is software/observability becoming a better AI bet than hardware now?

Curious what people here think, especially anyone following hyperscaler capex, networking, or inference trends closely.

https://preview.redd.it/o8xgssvr5rzg1.png?width=1254&format=png&auto=webp&s=4095fae432f68ba31c8a538570d3d1bc08ea6213

She’s proud of you. Congrats

I ported half of my HSA into INTC at ~$20. Is this how health insurance is supposed to work?

Buy calls retard, we are going a lot higher for some more months.

https://preview.redd.it/pfqq56l3brzg1.png?width=1024&format=png&auto=webp&s=0d646207c09fefd3613e983348d94a2b469ffbc8