The macro landscape is clear to anyone paying attention. The conflict in the Middle East has effectively shuttered the Strait of Hormuz, and despite the persistent narrative regarding diplomatic off-ramps, those channels are currently non-existent. This is not a temporary logistical hiccup; it is a structural impairment of global energy transit.

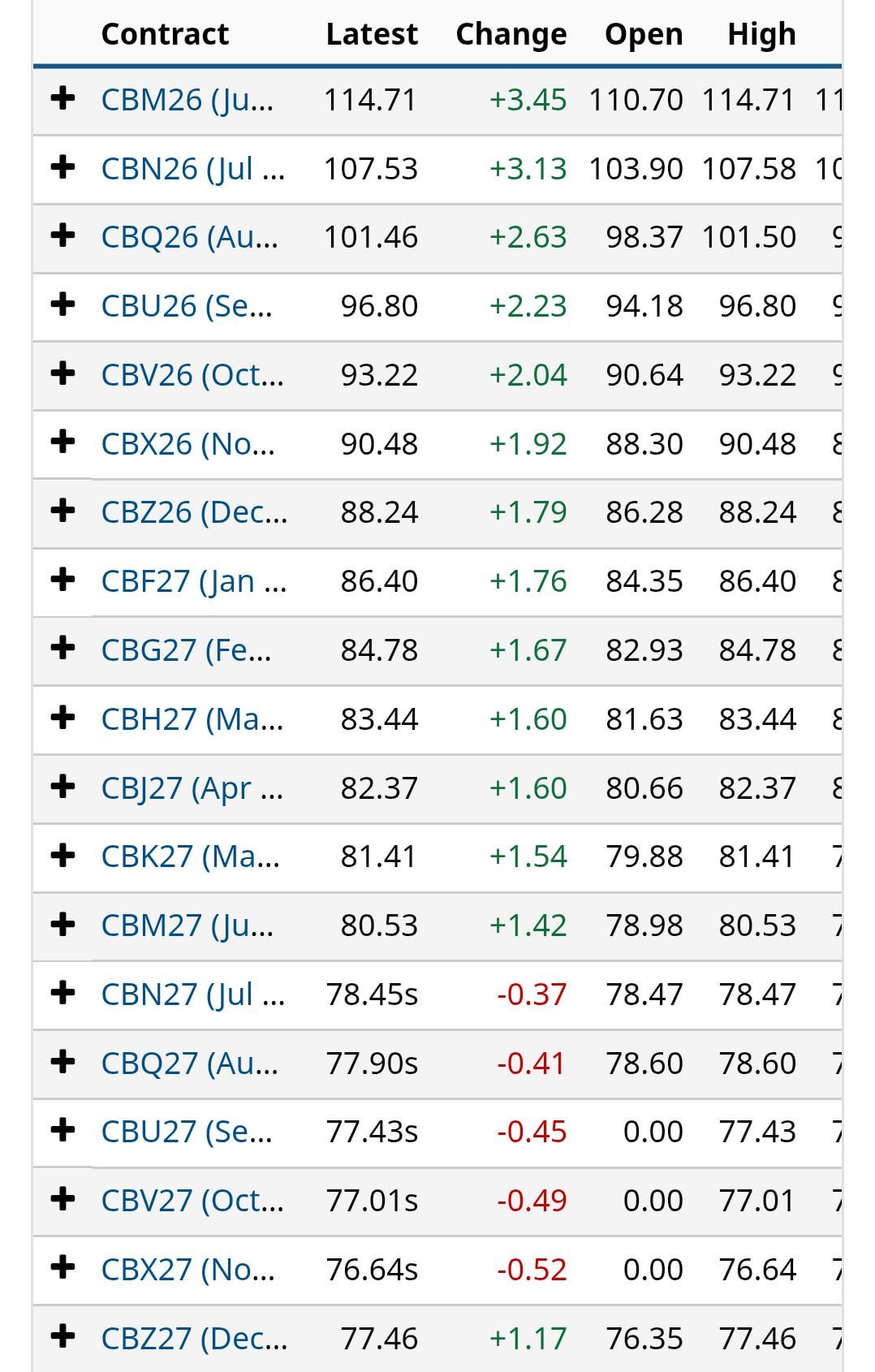

Take a look at the attached futures strip. The paper market is suffering from a massive disconnect. While the front-month contracts reflect the immediate panic, the back end of the curve is in deep backwardation. The market is pricing in a scenario where this conflict resolves by late summer and global supply chains immediately revert to a pre-war state.

That is an exercise in delusion. Conflicts of this scale do not resolve on such convenient timelines, and the physical infrastructure damage and insurance premiums alone will create a long-term floor for prices. The paper traders are entirely mispricing the medium-term supply constraints. When the institutional money finally capitulates and realizes this is a multi-year supply deficit, the back end of this curve will undergo a violent re-rating.

The Strategy: Unhedged Torque and Offshore Assets

Playing a structural deficit requires moving away from integrated majors and into offshore drillers and mid-cap E&Ps with significant unhedged exposure to the commodity. Drillship day rates are expanding rapidly, and operators like Valaris, Seadrill, and Noble are rapidly transforming into free cash flow machines as they re-price their fleets into this environment.

My portfolio is currently up +85.83% on the open, with a total market value of 1.25M DKK ($195,680 USD at today's exchange-rate).

Positions Disclosure

I am heavily levered into offshore drillers and energy names, holding until the institutional market aligns with the reality of the supply deficit.

Valaris (VAL): 190 shares @ $43.55 Current: $101.97 (+134.14%)

Kosmos Energy (KOS): 11,167 shares @ $1.307 Current: $2.960 (+126.47%)

Seadrill (SDRL): 351 shares @ $24.44 Current: $49.79 (+103.72%)

Noble (NE): 339 shares @ $25.33 Current: $50.98 (+101.26%)

Chord Energy (CHRD): 100 shares @ $85.13 Current: $140.23 (+64.72%)

SM Energy (SM): 478 shares @ $17.96 Current: $29.28 (+63.03%)

Crescent Energy (CRGY): 1,200 shares @ $8.11 Current: $13.07 (+61.16%)

GeoPark Ltd (GPRK): 1,320 shares @ $5.96 Current: $9.25 (+55.20%)

Matador (MTDR): 236 shares @ $39.96 Current: $61.13 (+52.98%)

FTAI Infra LLC (FIP): 1,870 shares @ $4.21 Current: $5.58 (+32.54%)

Murphy Oil (MUR): 386 shares @ $30.55 Current: $40.03 (+31.03%)

SunCoke Energy (SXC): 1,790 shares @ $6.470 Current: $6.740 (+4.17%)

Comstock Resources (CRK): 606 shares @ $19.24 Current: $17.29 (-10.14%)

Banned Ticker (XXX): 3,000 shares @ $2.50 Current: $0.64 (-74.40%)

DKK/USD: Short 81,553 @ 0.1565 (Flat) Represents leverage in the portfolio

The geopolitical risk premium is currently underpriced in the deferred months. The structural deficit is a reality that the current curve has yet to accept. Position accordingly.

https://i.redd.it/qzrhw1bes3yg1.jpeg

Posted by Leveraged_Lots

6 Comments

Interesting post thanks. Which names do you like the most? I rarely play the energy sector

Two things affect pricing. Demand and supply.

The drop on oil futures price is NOT the market expecting supply to recover.

It is due to the

market pricing the destruction of Demand.

That’s a lot of words, but I must remind you that stocks only go up.

whats the banned ticker?

Sorry i recently ran out of crayons to eat.. what does SoH mean?

👆 This guy thinks he’s smarter than the market.