Wendy’s closed today at $6.96, resulting in a market cap of approximately $1.33 billion.

That is an unusually low valuation for a company with $2.18 billion in TTM revenue, consistent free cash flow, and a brand that has been part of American culture for over 50 years. 🇺🇸

Updated Valuation Snapshot

• P/E (TTM): ~8.1x

• P/S: 0.61x

• Dividend yield: ~8.1% (annual dividend of $0.56 with a well-covered ~66% payout ratio)

• Enterprise value: ~$5.4 billion (including ~$4.1 billion net debt)

The company also carries roughly $908 million in owned real estate on the balance sheet. While Wendy’s is not a pure real-estate play like McDonald’s, these properties provide meaningful downside protection, steady rental income from franchisees, and potential for future value creation through optimization or sale-leasebacks.

Why the Valuation Looks Out of Step

At $1.33 billion, Wendy’s trades smaller than several unprofitable or early-stage tech/SaaS companies that most Americans have never heard of. Names like Asana (~$1.48B) and Upwork (~$1.40B) carry similar or higher market caps despite lacking Wendy’s brand recognition, revenue scale, profitability, and high dividend yield. The market is currently pricing a nationally recognized fast-food icon like a distressed micro-cap while rewarding speculative software names with premium multiples.

The Business Is Built to Last

Wendy’s is a mature, cash-generative franchisor (95%+ franchised locations) with a durable moat: square never-frozen beef patties, the Dave Thomas legacy, and a brand that resonates across generations. This is not a fad company. It has weathered decades of competition and economic cycles, and the name recognition alone gives it staying power that many newer concepts lack.

On top of that, international expansion is accelerating and represents a genuine long-term growth driver:

• Wendy’s already operates over 1,400 restaurants in 35+ international markets.

• The company is targeting 2,000 international units by 2028, with 70% of near-term net unit growth coming from outside the U.S.

• Recent deals in Mexico, Italy, Armenia, and other regions show disciplined execution. International same-store sales have been notably more resilient than the domestic side.

Combined with the owned real estate assets and the high dividend, this creates a stable base that the current stock price largely ignores.

The Setup

The stock has been under pressure due to soft same-store sales and a cautious 2026 outlook. That weakness is real and explains the depressed valuation. However, much of the bad news appears priced in at these levels. With an 8%+ dividend providing income while you wait, a resilient brand, owned real estate for balance-sheet support, and accelerating international growth, the risk/reward skews favorably for investors with a longer horizon.

It is a high-quality, cash-flowing American franchise that has been beaten down to levels that look disconnected from the underlying business fundamentals.

Bottom line

At $1.33 billion market cap, Wendy’s offers a rare combination of brand durability, international expansion potential, real estate value, and a generous dividend — all at valuations typically reserved for struggling or unproven businesses. The asymmetry is attractive for patient capital.

Not financial advice. Always do your own research.

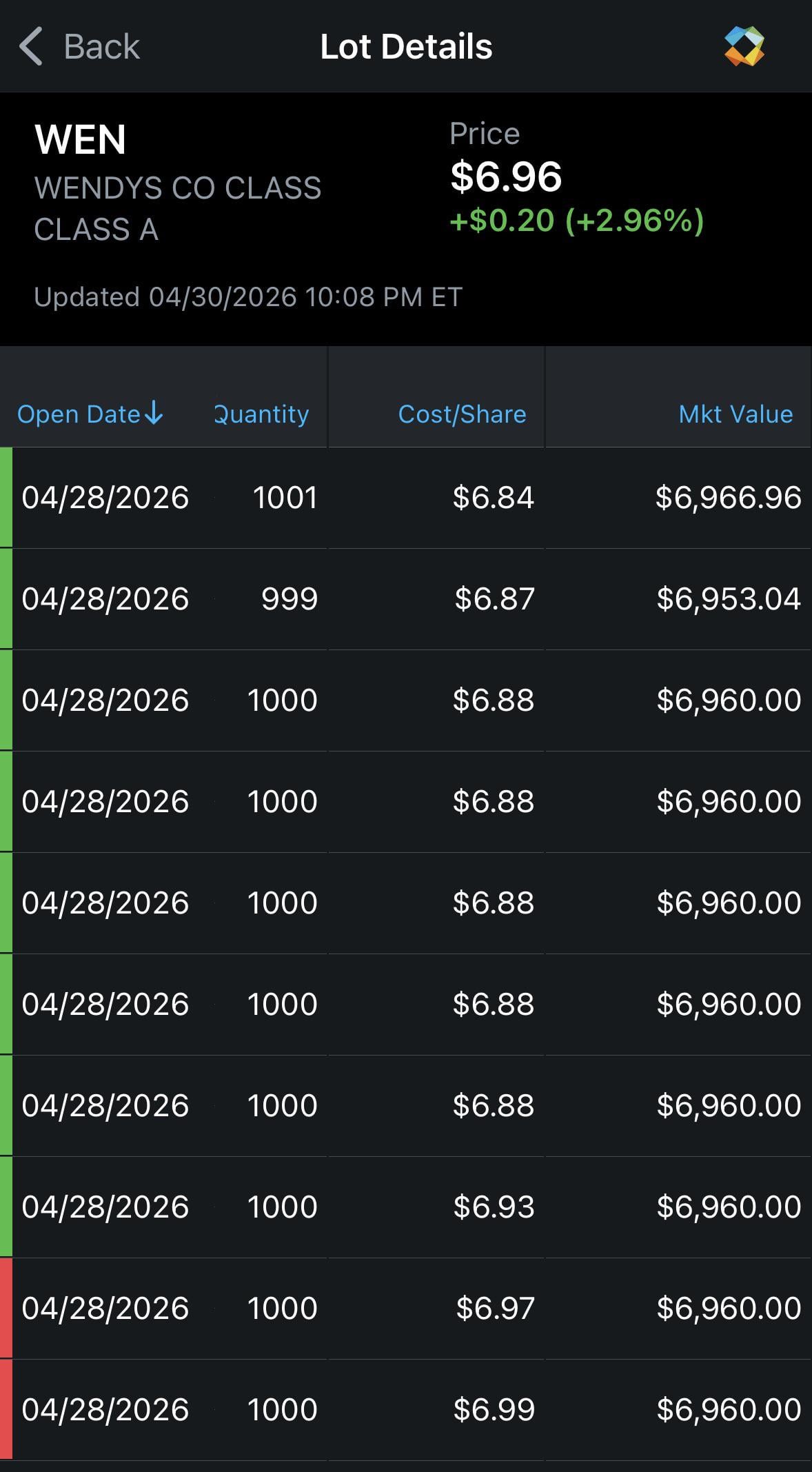

My position: 10k shares @ $6.90 avg

https://i.redd.it/qwx175oypfyg1.jpeg

Posted by movehoe

18 Comments

Fools with.. wait baconators yummy

Not reading all that

Just make sure you put the fries in the bag bro

I don’t have 69k but Im in..

If this goes belly up I’ll be out of a job too. Fuck it I’m in.

AI slop promoting edible slop

Haha! Wen… DD 😃

But seriously though, stop with that slop.

I like the stock. Let’s go!

You’re not going to discuss the massive debt at all? It’s kinda the driver for the distressed price.

You’re betting on management executing a big turnaround before the debt wipes them out. I’d also anticipate that dividend gets slashed sooner than later.

Wendy’s used to be a great one but their current management team needs to be rebuilt.

They are now doing chili in a can and “fresh” beef patties.

They need to get back to the biggie bag being a value, the pretzel bun burger. Lower your prices and focus on being a dividend stock.

And I own a couple hundred shares so…I hope they fix their shit

Be sure to tell the manager you did this when you’re applying there next month.

insane waste of capital but could be solid mid to long term

Debt is 4x the market cap… did I read that right?

You like $WEN deez nuts drag across your face?

Idk man, I am in my late 20s and even among my own age group that grew up with Wendy’s, everyone I know would only go to Wendy’s if it was the only place open / nearby.

I’ve never even see my younger cousins who are 16, 14, and 12 eat Wendy’s, though I’ve seen them eat McDonald’s, Taco bell, Subway multiple times.

Even when I do go to Wendy’s the average client is some disheveled middle aged individual ordering shit off the value menu.

It’s a Ronald McNopoly kind of world nowadays, dunno.

Who goes to Wendy anymore ?

Debt is high… But they pay a great dividend and seemingly print cash. Definitely a buy.

Shit went downhill. Used to be the best. Just open Google maps and type Wendy’s and go to 10 random ones around the country and see the reviews. Here’s one I found lol

https://preview.redd.it/686gkpnpggyg1.jpeg?width=1080&format=pjpg&auto=webp&s=4e0cd1542a45997a5a842887eb18873167edef33