TL;DR

Macro cooked, inflation immortal, multiples pricing in the singularity = short.

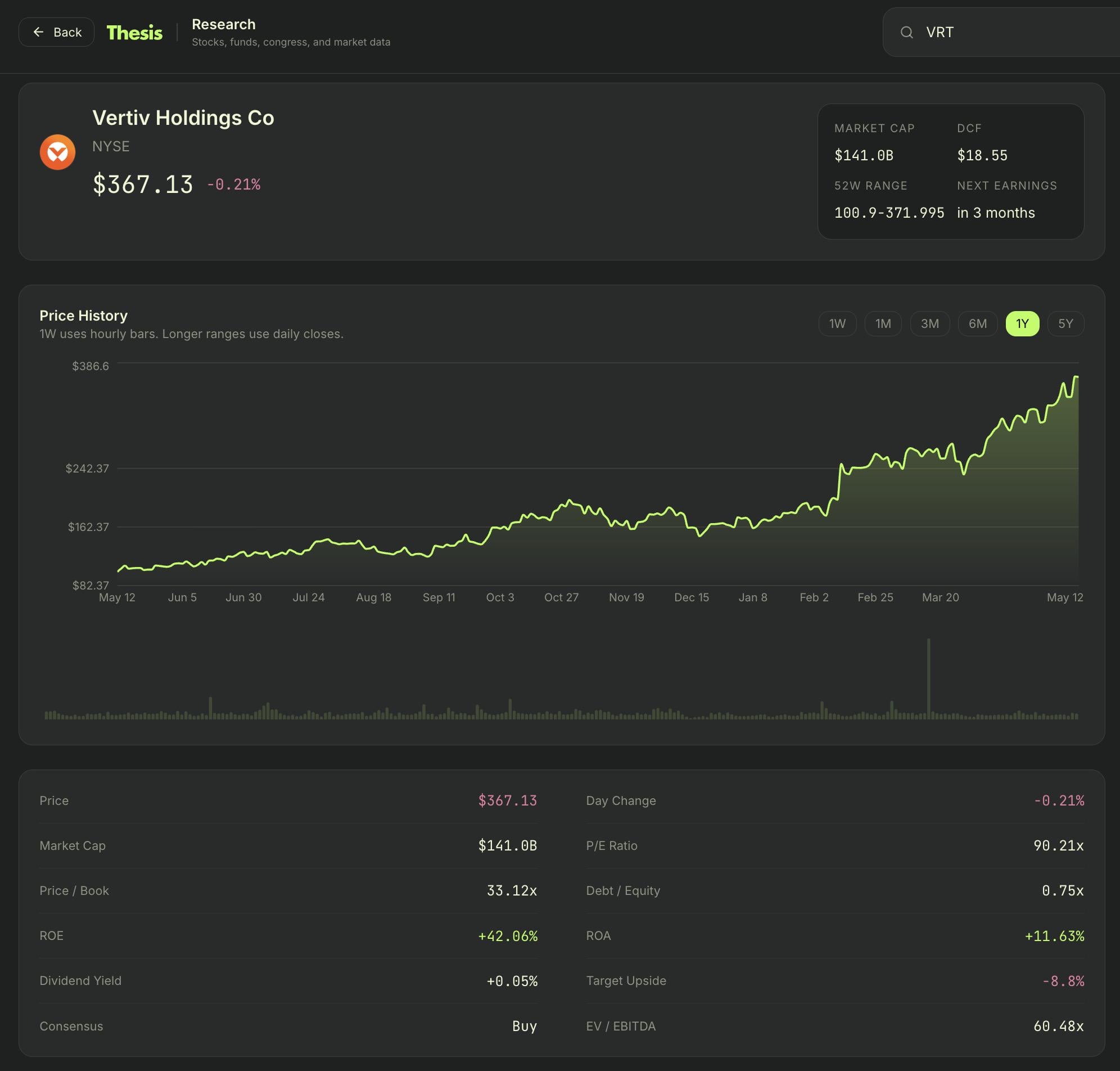

Vertiv ($VRT) is a ~90x trailing P/E electrical equipment company servicing AI capex build. Business is real (+30% YoY revenue, 42% ROE). The multiple is the trade. Consensus PT ($335) is already below spot ($367). Expressing the bear via a Jan 15, 2027 340/260 put debit spread.

The thesis in 4 bullets

• VRT short is a price expression, not a business expression. Industrial peers (ETN, HUBB, nVent) trade 20-30x. A re-rate to 35-40x forward (still premium) = $180-220 stock. ~40-50% down with zero change to fundamentals.

• Hyperscaler capex is the load-bearing wall. MSFT/META/GOOG/AMZN/ORCL + CoreWeave are most of the order book. One "digesting capacity" comment cracks the forward multiple.

• Energy spike. Higher power prices compress hyperscaler AI ROI → capex slows. This shows up in the numbers in a few months. We're already energy-constrained vs. capex.

• Reflation is mechanical. β=2.10, long-duration equity priced on terminal AI growth. 10Y back to 5% and this leads the drawdown. The AI infra basket (VRT/CEG/VST/ANET/SMCI) trades as one ticker on rate days.

Probability-weighted 12-month target: ~$250-280 (-25 to -30% from spot). Asymmetry: +30% if everything works, -40-60% if anything cracks.

____

What VRT actually is

A cooling and power infrastructure company (Liebert thermal, Geist PDUs) that the market has decided is a pure AI data center derivative. Real earnings, real revenue growth (+30% YoY), real customers. Not a fraud, not PLTR.

The problem isn't the business. The problem is the price.

The setup:

Price

$367

P/E (TTM)

~90x

EV/EBITDA

~60x

Beta

2.10

Consensus PT

$335 (below spot)

Industrial peers (ETN, HUBB, nVent)

20-30x

12-month price scenarios:

Scenario

Probability

Target

What happens

Bear (base)

40%

$200-240

One hyperscaler guide-down, inflation sticky, macro breakdown

Severe Bear (3 vectors fire)

25%

$130-170

Capex slows + oil shock + reflation

Muddle

15%

$300-380

Nothing ever happens, Anthopic + OAI IPO's go well

Bull

15%

$420-500

Capex accelerates, rates ease, blow off top

Megabear (everythings fucked, 2008, call your mom, im rich dont call me)

5%

$80-120

Capex cancellations, Recession, Oil $200+, Raised rates

The Structure: Jan 15, 2027 340/260 Put Debit Spread

Picked Jan over Nov 2026 for the OI. Nov 340 has 2 contracts of open interest — unfillable at the mid. Jan'27 340 has 30, the 260 has 250. Paid up ~7% on debit for liquidity I can actually exit into.

Leg

Strike

Mid

Delta

Long Put

340

$58.83

-0.32

Short Put

260

$26.00

-0.17

• Net debit: $32.83/sh → $3,282 per spread

• Max gain: $4,718 per spread (at ≤$260 expiry)

• Max loss: $3,282 (the debit)

• Break-even: $307.18 (-16% from spot)

• R:R: 1.44:1

• Net Greeks: Δ -15 / Vega +21 (slightly long vol) / Theta ~-$0.13/day per spread

Not financial advice. Will prob lose all my money.

Edit: grammer.

Edit 2: for people who keep DMing me the screenshot is from Thesis . Not affiliated.

https://i.redd.it/l18mp52b2s0h1.jpeg

Posted by CCforWork

1 Comment

See the problem with with this is that it’s solid dd and makes sense logically. It’s just not that kind of market rn